The Dilemma: Speed vs. Control

The digital wealth management market is exploding. By 2027, the robo-advisory sector is projected to manage trillions in assets. For fintech founders and CTOs, the opportunity is massive. However, the path to entry is fraught with technical decisions.

Your biggest hurdle isn’t marketing; it is choosing the right Robo-Advisor Tech Stack. Do you leverage an existing giant like Betterment? Do you buy a turnkey white-label solution? Or do you build a proprietary Custom AI engine from scratch?

This decision dictates your time-to-market, compliance burden, and long-term valuation. This guide breaks down the three primary paths to help you decide.

Option 1: Utilizing APIs (e.g., Betterment)

Leveraging a Banking-as-a-Service (BaaS) or Investing-as-a-Service (IaaS) API is the middle ground. You utilize the infrastructure of a regulated entity but build your own front-end user experience.

Betterment for Advisors and similar APIs allow you to offload the heavy lifting. They handle trade execution, rebalancing, and custody.

Pros:

- Faster Launch: You can go to market in months, not years.

- Regulatory Cover: Often, the provider handles custody and some compliance aspects.

- Reliability: You are building on tested infrastructure.

Cons:

- Fee Sharing: You must split revenue with the API provider.

- Limited Logic: You cannot easily alter the core trading algorithms.

Option 2: White-Label Solutions

White-label platforms offer a “business in a box.” You get a fully built back-end and front-end, rebranded with your logo. This is common for traditional banks wanting to add a digital arm quickly.

Providers often supply pre-made portfolios and onboarding questionnaires. You simply turn the key.

Key Features:

- Turnkey Interface: No need for extensive UX/UI design.

- Standardized Portfolios: Proven investment strategies included.

- Support: Vendor manages maintenance and updates.

The Downside: differentiation is difficult. If your competitor uses the same white-label provider, your product will look and feel identical. You are competing solely on brand, not technology.

Option 3: Custom AI Development

This is the path for true disruptors. Building a Custom AI solution means developing your own proprietary algorithms for asset allocation, tax-loss harvesting, and risk assessment.

This approach requires a robust engineering team. You will need data scientists, Python developers, and rigorous testing.

Why Build Custom?

- IP Ownership: You own the code and the algorithm, increasing company valuation.

- Unique Value Prop: You can offer niche strategies (e.g., ESG-focused AI, crypto-hybrid models) that APIs don’t support.

- Cost Control at Scale: You avoid paying high basis-point fees to vendors once you scale.

The Risks:

- High Upfront Cost: Development can cost hundreds of thousands.

- Compliance: You are solely responsible for regulatory adherence.

Comparative Analysis: Making the Right Choice

Choosing your stack depends on your business goals and budget. Let’s look at the trade-offs.

| Feature | Betterment API | White-Label | Custom AI |

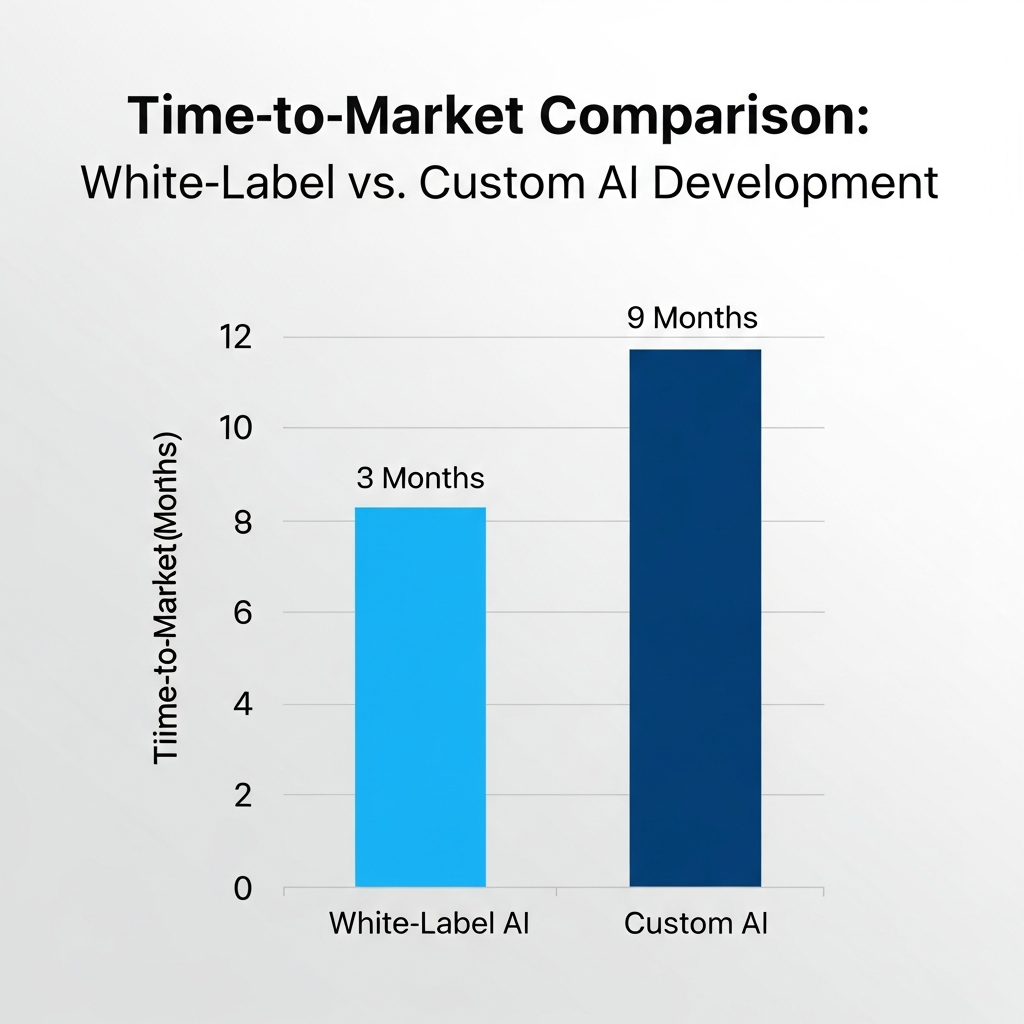

| Time to Market | Medium (3-6 Months) | Fast (1-3 Months) | Slow (9-18 Months) |

| Cost | Medium Setup + Rev Share | Low Setup + Licensing | High Upfront CapEx |

| differentiation | Moderate (UI only) | Low | High (Core IP) |

| Tech Talent Needed | Front-end Devs | Minimal | Full Stack + Data Science |

Statistical Reality: According to recent industry data, over 60% of fintech startups fail due to running out of cash before finding product-market fit. This statistic suggests that starting with an API or White-Label solution to validate your market, before pivoting to Custom AI, is often the safest bet.

Future-Proofing Your WealthTech Platform

Regardless of the stack you choose today, you must plan for tomorrow. The wealth management industry is shifting toward hyper-personalization.

Basic robo-advisors just balance portfolios based on age. The next generation uses Generative AI and machine learning to analyze spending habits and predict life goals.

Integration Matters: Ensure your stack can integrate with other tools. You will need connections to CRM systems, KYC (Know Your Customer) vendors, and banking data aggregators like Plaid.

Real-World Example: Consider Wealthfront. They started with standard passive investing. Over time, they built proprietary “Self-Driving Money” technology. This custom automation is now their primary differentiator, something they could not have achieved with a rigid white-label solution.

Conclusion

There is no single “best” robo-advisor tech stack.

If you are an RIA needing a digital portal, White-Label is likely sufficient. If you are a fintech startup needing speed but some UI control, an API like Betterment is ideal. However, if you aim to reinvent wealth management with unique algorithms, Custom AI is the only path.

Assess your budget, your timeline, and your desire for IP ownership. Make the choice that aligns with your exit strategy.

Ready to Transform Your Fintech Strategy?

Stop wondering and start transforming. Contact Sociazy’s expert team today for a no-obligation consultation on how we can solve your specific WealthTech challenges.